Do you have a Personal Umbrella policy?

If you’re like a lot of people, you probably don’t. You might not even know what a Personal Umbrella policy is.

A Personal Umbrella policy is an insurance policy that gives additional coverage to you if you have a claim that is larger than your home or auto insurance policy limit.

You can kind of think of it as a little extra peace of mind.

As an insurance agent, I write personal insurance policies for people every day. And it surprises me how many people don’t have this coverage in place.

When I bring up this coverage, my clients generally ask me the same 5 questions.

- What is a Personal Umbrella policy?

- What does a Personal Umbrella policy cover?

- What are the risks of not having this type of policy?

- How much does a Personal Umbrella policy cost?

- What keeps people from buying a Personal Umbrella policy?

To help answer these questions, I’ve put together this short guide. Read on for the answers to the top 5 questions I get about Personal Umbrella Insurance policies.

What is a Personal Umbrella policy?

A Personal Umbrella policy is an insurance policy that covers the insured when the limits from their other insurance policies have been fully paid out.

Here’s an analogy to help you understand this coverage.

Imagine you are outside on a rainy day. You have on your rain boots, a raincoat, and even water-resistant pants. In addition, you’re carrying a huge umbrella. Your boots, coat, and pants are your primary protection from the rain. Your umbrella is just extra protection – covering what wasn’t covered by your other rain gear.

In regards to insurance, your homeowner policy, auto policy, and maybe a motorcycle policy are your first line of defense – your primary coverages. These policies are like the rain gear you were wearing in the analogy.

An umbrella policy is additional coverage to protect you if you find yourself vulnerable to a claim that was too big to cover by one of your primary insurance policies.

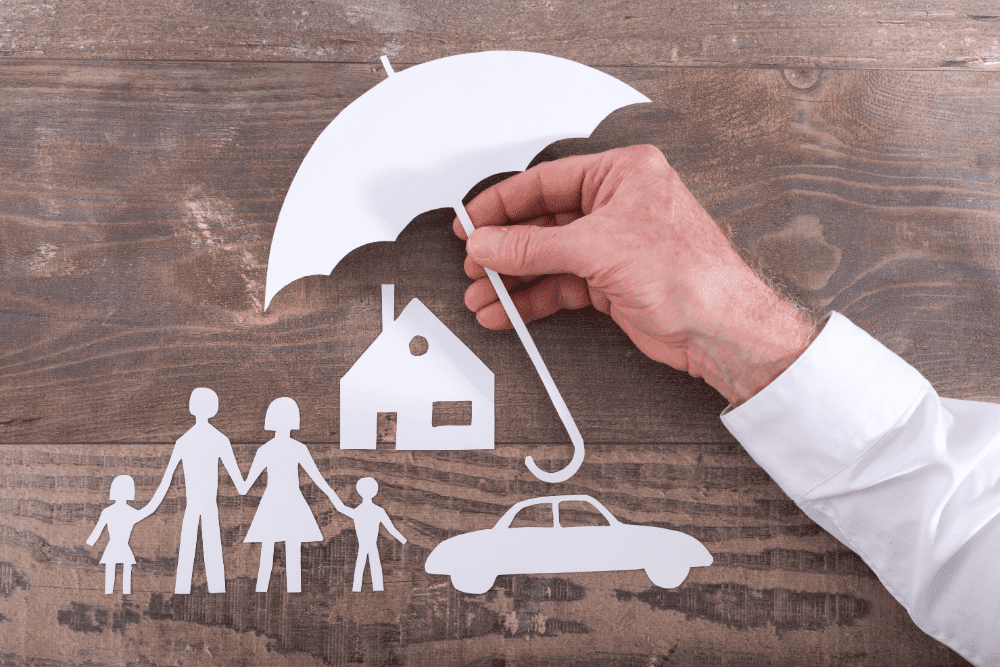

And this “umbrella” covers your auto policy, your homeowner policy, your motorcycle policy, your motorhome policy, and any other personal policy you have in place.

What does a Personal Umbrella policy cover?

Now let’s get practical for a minute, so you can see exactly how this kind of policy works.

Imagine you are in an auto accident. You are responsible for hitting another vehicle. Unfortunately, the accident caused the other driver to need significant medical care.

The other driver ended up with spinal problems which required extensive surgery. It also kept the driver from being able to work for several months. The claim gets turned in to your insurance and by the time it is all wrapped up it’s near $500,000.

Your auto insurance policy has a $100,000 limit for Bodily Injury. Who is responsible to pay the additional $400,000 to cover the claims?

You are.

Here’s another example. One sunny afternoon, the mailman opens your front gate to drop off a package. What she didn’t know is that your dog is unchained.

Taken by surprise, your dog, who is not friendly to strangers, lunges at the mail carrier and bites her in the face.

Over the next few months, the mail carrier ends up needing multiple hospital stays, several reconstructive surgeries, and prescription medications. The medical bills amount to over $400,000.

The claim is submitted on your homeowner policy. However, your medical liability limits will only cover up to $300,000. Who will pay the extra costs?

You will.

If you have a Personal Umbrella policy, it will cover the additional costs that your auto, homeowner, or other personal insurance products won’t cover.

What are the risks of not having a Personal Umbrella policy?

If you find yourself in a situation like the ones above, you can be held responsible for covering the additional costs. And if you don’t have the resources to cover the costs, you will most likely face litigation.

If you do end up in litigation, the consequences can be far-reaching. You may lose your personal or business assets.

How much does a Personal Umbrella policy cost?

Personal Umbrella Insurance is rather inexpensive. For instance, for $1 million in coverage, you can expect to pay $380 per year.

What factors impact the cost of this coverage?

The cost of a Personal Umbrella policy will depend on these four factors:

1. The number of underlying policies

Like I said earlier, a Personal Umbrella policy covers all of your other personal insurance policies. The cost of your policy will depend on the number of policies that will fall under your Personal Umbrella policy.

If you only have an auto policy, you can expect your Personal Umbrella policy to be less expensive. If you have an auto policy, a homeowner policy, a boat policy, and a policy for your ATV, you can expect your Personal Umbrella policy to cost more.

2. Age of the drivers on your auto policy

If your Personal Umbrella policy covers your auto policy, the age of your drivers will be a factor in determining the price of your policy.

If you have drivers under the age of 25 on your policy, it will cost more. Also, if you have elderly drivers on your policy, you can expect to pay more.

3. Number of drivers on your auto policy

Another factor that will impact your premium cost is the number of drivers on your auto policy. The more drivers, the more expensive your insurance will be.

4. Number of vehicles on your auto policy

The final factor is the number of vehicles insured on your auto policy. The greater number of vehicles, the more expensive your Personal Umbrella policy will be.

What keeps people from buying a Personal Umbrella policy?

As an insurance agent, I’m often surprised by how many people don’t take advantage of this important coverage. Generally, people give me two responses when asked why they don’t have this coverage in place:

1. “I didn’t realize I needed it.”

Many people don’t know that they are open to possible litigation because of a claim larger than their other insurance policy limits. They don’t know that they are exposed.

2. “I don’t think that will happen to me.”

The other common response is that many individuals just don’t feel like these types of situations are likely to happen to them. In essence, they are willing to risk the potential of having an accident that exceeds their insurance policies limits.

Still not sure you need this coverage?

Maybe after reading this article, you’re still not sure you need this coverage. And I can tell you that you’re not alone. Many people decide to hold off on purchasing this coverage.

So is there anything I can say to change your mind?

I have to be honest with you, I don’t often see my clients rely on their Personal Umbrella policy. We can be grateful that extreme incidents don’t often happen.

However, they do sometimes happen. Many people in this world thought it wouldn’t happen to them… until it did.

And while these incidents don’t happen often, when they do happen they can be catastrophic! You can literally lose everything!

Like I said earlier, Personal Umbrella policies are inexpensive considering the coverage you are getting. And if you have young drivers, a lot of assets, or own a business, you are much more likely to face litigation if you are responsible for a major accident.

Also, if you have other liabilities like a trampoline or pool on your property, you are at greater risk.

Personal Umbrella Insurance policies are inexpensive. And, getting a quote is absolutely free. It costs you nothing to call in and find out what a Personal Umbrella policy will cost you.

At Baily Insurance, we sell all kinds of personal insurance products. These products bring our clients added peace of mind that they and their loved ones have the protection in place that they need.

If you are looking for that peace of mind, we can help you get coverage in place that you need. Give us a call today!

For other helpful articles about your insurance, check out:

12 Factors That Affect Your Auto Insurance Cost

What Does Homeowner Insurance Cover? Most Popular Questions Answered